In a previous blog post, Aaron Ayusa, Baton Systems’ Director of Client Success, detailed how data obtained from the process of real-time reconciliation can be harnessed to optimise intraday liquidity management. But cash management and operational efficiencies are not the only benefits to be derived from real-time reconciliation. Here, Aaron explains how the process can significantly improve the ability to mitigate counterparty risk and ultimately benefit the business as a whole.

Counterparty risk management – that is, the process of identifying, assessing, and mitigating the risk that a counterparty might default on its obligations – is important for several reasons, but primarily because it is a critical part of the process required to control the potential negative impacts of counterparties failing to fulfill their contractual obligations. Settlement risk, the risk that a counterparty fails to deliver against its final obligation, is a key component of counterparty risk and one that is increasingly on the radar of regulators and related stakeholders.

The settlement risk management processes of most banks rely on end-of-day account statements as a key source of information for the required reconciliation. This outdated legacy practice generates unnecessary delays and means that the day after Value Date (VD+1) is the earliest that a bank can be sure whether or not a counterparty has met its payment. In practice, it’s not uncommon for all of the key functions within a bank to be unaware for several days, or even weeks, after value date that a payment has failed. Meanwhile, the bank may have been continuing to make payments, in ignorance, to a counterparty that has failed to meet its own obligations.

The risk of paying out to a failing counterparty is therefore a very real risk, with financial, reputational and regulatory repercussions.

Why is reconciliation important?

Whether done in real-time or at VD+1, reconciliation is important because it pertains to the books and records of a financial institution: in order for the firm to function well, checks and balances need to be in place to ensure that all of its transactions are correctly accounted for.

When reconciliation is done in real-time rather than at VD+1, not only does a bank know immediately when a counterparty has met its obligation, or failed to pay, but it also has the ability proactively to track and follow up missed payments and to release its own payments quickly and confidently on the basis of accurate information. In short, based on the risk assessment in place for that particular counterparty, a decision can be taken on whether to release or hold a payment.

It’s common within banks for operations teams to be benchmarked on nostro breaks – i.e. discrepancies between actual and expected cash settlements. But they need to rely on legacy technology and manual processes in order to keep track in real-time of cancels, corrections, amendments, and replacements across multiple ledgers.

Banks rarely view nostro breaks from a counterparty lens perspective. But with real-time data at their fingertips, operations teams can improve their organisation’s counterparty risk management by assessing and monitoring client behaviour and employing the risk mitigation workflows that the internal credit risk management (CRM) team has designated for each counterparty in the event of failure.

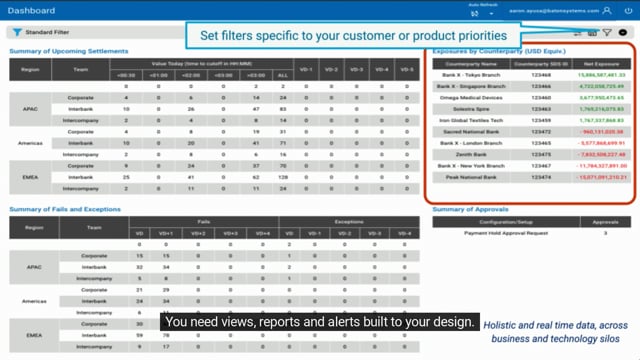

By pairing this information with analytics and automated workflows, banks have the ability to create a real-time update of settlement exposures based on outstanding receivables for each counterparty.

The information is not only valid in real-time but these data-driven insights can drive more informed decision-making for the following day as a firm assesses the next steps once it’s clear that a counterparty has failed, and indeed as limits and relationships are reviewed as part of the ongoing risk management cycle.

“When reconciliation is done in real-time rather than at VD+1, not only does a bank know immediately when a counterparty has failed to pay, but it also has the ability proactively to track and follow up missed payments and to release its own payments quickly and confidently on the basis of accurate information”

How Baton facilitates real-time reconciliation

Baton’s Core-Payments® solution streamlines this process and brings real-time connectivity, visibility and control to the settlement management process, integrating with a bank’s systems to consume settlement obligations and relevant payment messages. Core-Payments accelerates the reconciliation processes by reconciling inbound and outbound payments as they are received and sent, using Baton’s smart technology to assign cash flows against specific obligations and counterparties. Using this real-time data, Baton’s smart, automated workflows check, hold, or release payments according to configurable business rules.

Watch to learn how Core-Payments assess risk with live & historic data for counterparty, liquidity, operational & payment risk

With Core-Payments, banks can avoid breaching limits or paying out against a failing counterparty. Nostros can be managed more effectively, avoiding overdrafts or failed settlements, and manual processes (and the multiple associated risks) are significantly reduced. Baton’s rules-based framework for using real-time data, reconciling payments, and creating custom workflows, accelerates time to market, removes limitations and mitigates risk.

Core-Payments can be deployed as either a cloud-based or on-premises solution and can be integrated seamlessly with legacy systems and processes.

“Core-Payments reconciles inbound and outbound payments as they are received and sent, using Baton’s smart technology to match cash flows with counterparties. Using this real-time data, Baton’s smart workflows check, hold, or release payments according to configurable business rules”

Beyond the back office

The impact of inefficient counterparty risk management is not only felt by the middle and back offices. The settlement risk and control issues that arise from continuing to pay a failing counterparty quickly become a front office, risk and business leadership problem. A business that is seen not to be displaying strong controls over its payment processes will also be opening itself up to regulatory scrutiny and potential penalties.

The front office can also benefit directly from using real-time reconciliation as a basis for counterparty risk management and control. Banks with the ability to reconcile in real time can create conditional payments, also known as Payment-on-Payment (PoP). This allows them to effectively service clients with smaller settlement risk limits or no limits at all, such as fintech start-ups, which would usually be rejected by credit risk managers. By using real-time reconciliation and putting business rules in place that dictate that a client will only be paid on receipt of a particular payment from them, the risk of settlement default is eliminated.

This functionality allows the firm to grow its business by expanding its range of counterparties and servicing a new client segment – a win for the firm, its new clients, and the wider market.

“The front office can also benefit directly from using real-time reconciliation as a basis for counterparty risk management. Banks with the ability to reconcile in real time can create conditional payments, also known as Payment-on-Payment (PoP)”